Why does financial pressure appear to have so many people who did what they were told- worked hard, got educated, bought a home, saved to retire? In the case of Gen X, the issue is usually referred to as individual budgeting failure. This is better explained by the structural: a series of mainstream systems that pushed risk to the households exactly at the time this generation of children became adults, parents and at the time of peak earning years.

1. Recessions which occurred at the worst career time

Gen X got into the workforce at times when layoff and wage control was not a glitch to be considered but a consistent element in the economy. The Great Recession came at a time when most were in their mid-career, old enough to have mortgages and kids and young enough to require decades more income. Loss of a job at that point is likely to cause a ripple effect: retirement savings cease, emergency funds are depleted, and debt serves as the bridge that continues to grow longer than one expects. The long-term impact is not the loss of a year or two of income, but a permanently changed financial course.

2. Student debt that haunted the middle-aged

Education was sold as the surest ladder to financial security, but lots of Gen X borrowers had loan balances far beyond the youthful career stage, when debt is said to be easily handled. That weight influenced the daily decisions, whether to purchase a house, how much should be saved and whether to assist children in school. The profitability bonanza put an added sting: by 1990 to 2010, for-profit college enrollments shot up by 600 percent and the industry dependence on federal grants provided good motivation to engage in high-pressure recruiting. In the case of households, the outcome would appear to be credential that was purchased with real money but with an unaccompanied wage power.

3. The transition of pension-to-401(k) that turned workers into the plan managers of their own

Gen X was the initial massive generation that is likely to retire with security based on personal accounts instead of employer person pensions. The new change required markets, fees, and discipline of contribution fluency, which is seldom acquired in school and at work. Also, it implied that results would be time-sensitive: a slowdown in the market during contribution years would be manageable, whereas a slowdown during the job loss or caregiving years would be catastrophic. Retirement planning became a second job, only that it was not trained and the stakes were greater.

4. Interest rates were tightened by debt and unexpected costs

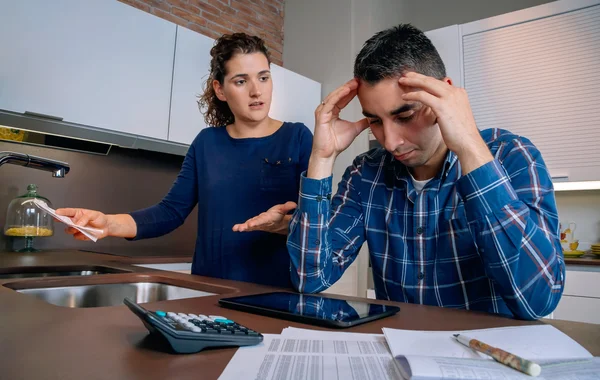

Even the motivated savers fell into a mathematical quandary: Rising necessities, increased out of pocket expenses, interest bearing debt had to compete with long term investing. When emergency funds were available, they regularly were compelled to do too much, to pay a medical bill one month and to fix a car the next. It is not that saving enough is absent in that setting, but rather a character flaw becomes less noticeable than an expected consequence of perpetual financial triage.

5. Nurturing that turned into a life phase of a determining cost

Gen X can be referred to as the sandwich generation since most of the adults are caring of children and also take care of the needs of aging parents. Such a task is not simply emotional work, but logistical and financial. Care giving will interfere with working hours, reduce employment opportunities and may rotate additional money as family needs. Retirement planning is once again the category that will be on the backburner since every other need of the person is urgent.

6. Whiplash in the homeownership in the wake of mortgage boom

The mortgaging products which seemed cheap initially and painful later were promoted as the foundation of the wealth of homeowner, although the road to acquisition in the 2000s had many pitfalls along the way. Prior to the crisis, about 80 percent of subprime mortgages in the U.S. were adjustable-rate mortgages and most of them had such characteristics as teaser rates and payment shocks. Refinancing and easy exits had vanished when the prices ceased to increase. It was not only foreclosures that were hurt but also the lost equity, blocked moves and a permanent mistrust of the housing ladder.

7. Salaries that were increasing on paper and reducing in the life of reality

Gen X have lived most of their adult years in an economic system where income growth did not tend to match housing, health, child care and college, university costs. It turned into a financial narrative of never-ending catch-up: advancements that are got up in rent increases, bonuses that are eaten up by insurance premiums, side jobs that now take the place of a full-time occupation. With time, this fades the sense of work providing a consistent effect of stability even in those whose work is a consistent, skilled, job.

8. Expensive short term credit that turns cash crunch into a whirlwind

Emergencies are costly when there are tight budgets. Payday loans are meant to be used on such an occasion: money now at the cost of high interest. A common fee system suggests 400 to 1000 percent of yearly charge as stated in a Journal of Economic Perspectives summary of pay day lending. To the borrowers, the threat is not the loan itself but the repetition of lending – the next paycheck will be used to settle the last bad time and the next bad time will silently be waiting in queue.

9. Perpetual contracts were sold as upgrade contracts

A few economic pressure comes in the form of vacation clothes. The growth of timeshares boomed past 1980, and most contracts were designed so that they produced an obligation of long-term payments whether the owners could use their purchase or not. Description of industries focuses on the way in which perpetual agreements became the center of the model, in which the owners continue to pay fees. In already debting and caregiving households, an easily unwindable contract may become an unspoken, long-range bleeding sore.

What unites these pressures is not misfortune or personal infirmity. It is a trend of downstream risk shifting where the institutions are spread to households until the average family became the shock absorber. Gen X never read the rules wrongly as much as they change in the middle of the game and then they are informed that it is their personal responsibility to read the scoreboard.